Por Bárbara Anderson

Cada cliente de Telcel dona 1,424 pesos por año a Carlos Slim

Se cumplen 10 años de la Reforma de Telecomunicaciones y América Móvil continúa como jugador preponderante. Sus tarifas mexicanas son el doble que en el resto de Latinoamérica. Telcel gana un extra cada año de sus clientes equivalente a 6,384 mdd.

De este tamaño es el ‘Costo Slim’.

¿Cuánto nos cuesta tener en México a un operador cuasi monopólico en el negocio de la telefonía móvil como es Telcel? Si, leyó bien, ¿cuánto dinero, mes a mes le entregan extra quienes tienen sus planes de telefonía e internet móvil contratados a la empresa de América Móvil? ¿Cuál es el ‘costo Slim’?

Una forma de medirlo es de manera individual, calculando cuántos pesos le depositan a la empresa los clientes de Telcel, más allá del paquete que tengan contratado. Y no son pocos, ya que la compañía que concentra 7 de cada 10 pesos de los ingresos del sector de telecomunicaciones móviles valuado en más de 300,000 millones de pesos (mdp) anuales[1]. Para poner en contexto, Telcel es cuatro veces el tamaño de sus competidores.

Estos cálculos son interesantes como referencia a los 10 años de la promulgación de la Reforma en Telecomunicaciones (10 de junio de 2013). Si bien México fue pionero en la implementación de estos cambios en competencia en América Latina, sigue siendo el único caso donde -sobre todo en los últimos años- Telcel, ha aumentado su tamaño concentrando el 73% de los ingresos del sector[2].

El ‘costo Slim’ es el peso que representa para la economía mantener un operador cuasi monopólico que le permite ubicar a México como uno de los mercados con los servicios de telecomunicaciones más caros en América Latina y sobre todo en telefonía y banda ancha móvil (BAM). Tanto que, casi la mitad de lo que pagan los usuarios de Telcel es sobreprecio versus el promedio de tarifas en la región.

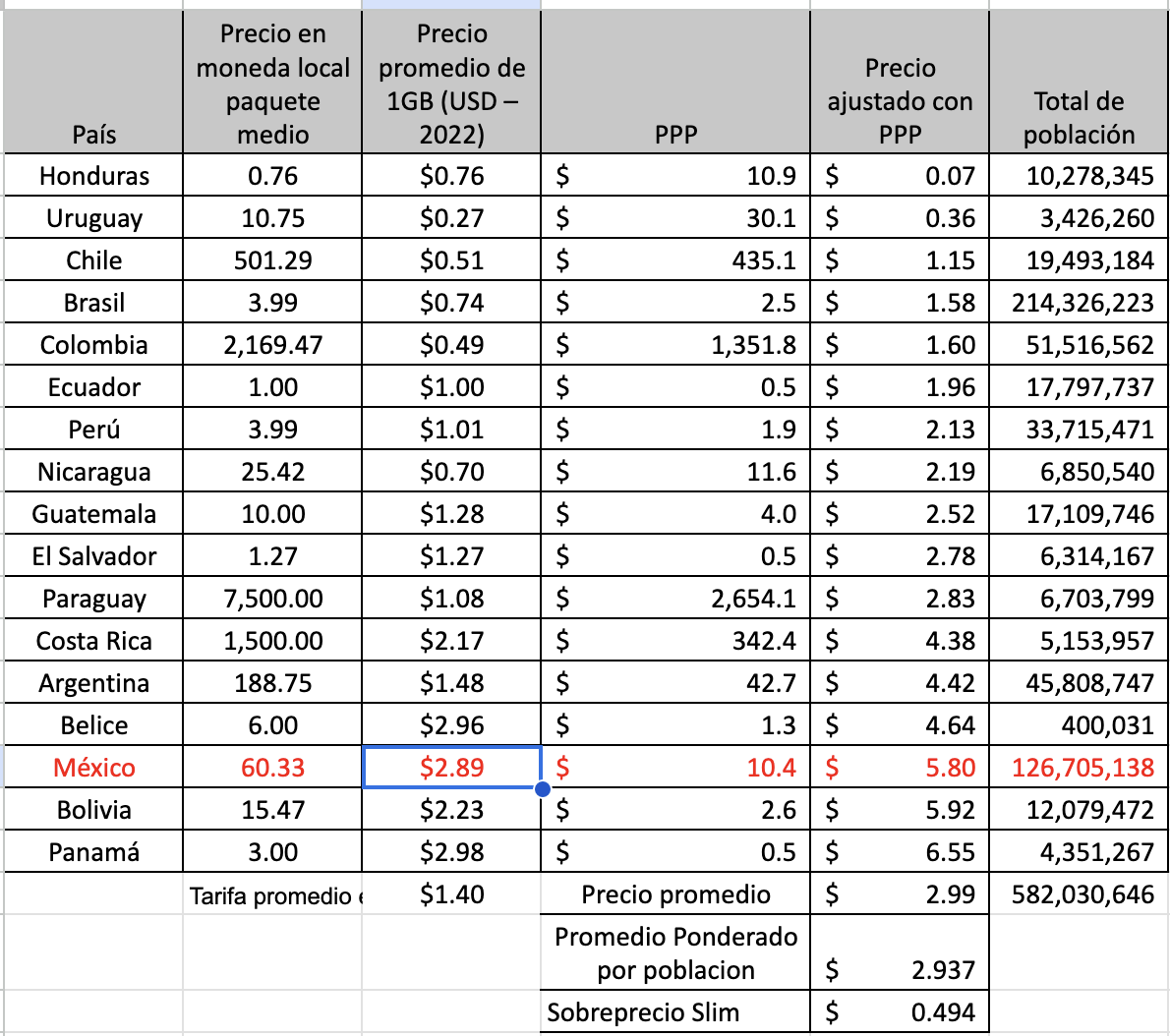

La agencia británica Cable.co.uk[3] publicó su ranking mundial 2022 con el costo medio de 1 gigabyte (GB) a nivel mundial. Para este listado utilizó la tarifa mediana de los planes de datos ofertados por país.

¿Cómo queda México frente al resto de los mercados más importantes de Latinoamérica? Una muestra medida en dólares en 17 países[4] revela que los usuarios mexicanos pagaron 2.89 dólares por GB, versus 1.40 dólares que le costó el mismo GB en promedio a los clientes en los demás mercados, es decir que, en precios nominales, el sobreprecio que tuvieron que pagar los usuarios locales fue de 48.4%.

Sin embargo, la manera más justa de comparar precios internacionales es ajustando estos valores según el poder adquisitivo, la capacidad de compra y la economía en cada mercado, es decir usando en todos los casos la paridad de poder de compra (PPP, por sus siglas en inglés). Las tarifas de Cable.co.uk, con ajuste del PPP más reciente del Banco Mundial[5], dan un resultado similar: 1GB en México cuesta en promedio 51.5% más que en cualquiera de los países vecinos.

Dentro de este número general promedio del mercado, ¿de qué tamaño es el extra de miles de millones de pesos que quedó en las arcas de América Móvil?

El dato es importante porque su firma Telcel concentra 7 de cada 10 clientes de estos servicios en el país.

El cálculo es simple: según su reporte anual 2022, Telcel tuvo a lo largo un promedio de 81.5 millones de usuarios. Ese mismo año, reportó ingresos por 225.4 mil mdp, es decir que cada uno de sus clientes le generó un ingreso de 2,765 pesos. Si a este monto le aplicamos el sobre precio revelado por Cable.com de 51.5%, quiere decir que esos millones de clientes aportaron un extra a Telcel de 1,424 pesos. Esta diferencia a favor de la empresa, multiplicada por todos sus usuarios, representa 114.9 mil millones de pesos, unos 6,384 millones de dólares. ¿A qué equivale el total de este cobro extra anual de Telcel? A montar cada 12 meses una gigafactory de Tesla, como la que se levanta en Monterrey.

El peso de Slim

Comparando país por país, tarifa por tarifa y ajustando los precios por paridad de poder de compra,

cada cliente de Telcel paga en promedio el doble por un gigabyte que cualquier otro usuario de

telefonía en banda ancha móvil en la región.

Fuente: www.cable.co.uk

*Tarifa promedio de cada gigabyte en 2022 en dólares, tarifas ajustadas por paridad de poder de compra (PPP, por sus siglas en inglés) en dólares. El data pricing se realizó con los costos por gigabyte de los paquetes medios de todas las operadoras. En México se evaluaron 26 planes disponibles.

Atentar contra el bienestar

Cobrar más por un servicio de uso masivo no solo es una cuestión de negocios sino que genera una pérdida de bienestar a nivel general en cualquier país.

En 2012 la OCDE publicó un estudio donde también se refería precisamente a la pérdida de bienestar atribuíble a la disfuncionalidad -hasta ese momento- de las telecomunicaciones en México. El organismo calculó que este sector operado por un cuasi monopolio y con precios excesivos versus otros países de la región, generaba una pérdida equivalente a 1.8% del PIB anual del país.

Jean Tirole, premio Nobel de Economía, en su libro ‘La economía del bien común’ se refiere a las desigualdades diferenciando entre aquella riqueza que se ha logrado a través de la innovación y creando valor para la sociedad y aquella riqueza que proviene de la extracción de rentas. Y cita como ejemplo a un discurso que dió otro economista francés, Philippe Aghion que en un evento explicó que “Carlos Slim es uno de los hombres más ricos del mundo, que ha hecho su fortuna gracias a estar protegido contra la competencia y no puede compararse con sus homólogos Steve Jobs o Bill Gates que han apostado por la innovación”. Tirole agrega que “un monopolio puede aumentar sus precios y, si lo hace hasta cierto límite, solo perder un escaso porcentaje de clientes. La empresa en posición dominante [...] no se privará de practicar una política de precios elevados o de ofrecer bienes y servicios de escasa calidad. De ello resulta un subconsumo y una disminución del poder adquisitivo para los ciudadanos. La entrada de competidores hace que aquellos estén menos cautivos y presiona sobre los precios”.

Slim no solo es usado por Tirole como ejemplo de lo que afecta un monopolio privado al desarrollo de un país. Francis Fukuyama en su último libro ‘El liberalismo y sus desencantos’, hace referencia a los peligros de llevar los programas neoliberales al extremo, donde la eficiencia de los mercados se convierte, explica, “en una especie de religión que se oponía por principio a la intervención del Estado. Se impulsó la privatización incluso en casos de monopolios naturales, como los recursos públicos clave, lo cual dió lugar a pantomimas como la privatización de la mexicana Telmex, donde un monopolio público de telecomunicaciones se transformó en uno privado, lo que facilitó el ascenso de uno de los hombres más ricos del mundo, Carlos Slim”.

En 2011, el ex secretario de Hacienda Carlos Urzúa evaluó en un estudio el impacto de los cuasi monopolios sobre el bienestar de los hogares mexicanos en diferentes deciles de ingresos. Allí detalló que los rubros a los que más se destina de manera proporcional el ingreso de los hogares son educación, energía y telecomunicaciones. "En el sector urbano la pérdida en el bienestar social representa, en casi todos los deciles, alrededor de la mitad del gasto promedio total de los hogares.”[6]

Preponderante que sigue preponderando

“La reforma ha sido la mejor década en el sector, los precios de los servicios de telecomunicaciones bajaron aunque no hubo ningún efecto en la competencia y sigue siendo un mercado altamente concentrado. Y la competencia no solo es para bajar los precios, sino para dar más servicios y más calidad”, explica Ernesto Flores-Roux, consultor en telecomunicaciones, “faltó una mejor aplicación de la preponderancia, menos medidas y priorizadas de tal manera que pudiera multar”.

Uno de los pilares de la Reforma en Telecomunicaciones fue determinar la preponderancia, el tamaño tanto de Telmex (con Telcel) como el de Televisa, para lo cual se redacta un manual de ajustes -con 160 obligaciones a cumplir- y se crea el Instituto Federal de Telecomunicaciones (IFT) para que llevara el control y timón de la nueva era. “Creo que esto no se hizo correctamente. La preponderancia debió contener menos medidas y priorizarlas de tal manera que los errores se pudieran multar. El documento de preponderancia tiene 1800 páginas y es tan complejo que el que mucho abarca poco aprieta. No era implementable, ni hay ningún órgano regulador que sea capaz de darle seguimiento a todo esto”, afirma Flores-Roux, “en México se decidió castigar al operador grande por ser grande y no por ser malo”.

En el resto de los países dónde opera América Móvil, y que también aplicaron años más tarde sus propias reformas pro competencia en telecomunicaciones, las empresas del consorcio de los Slim sí cedieron espacio de su negocio móvil y aumentaron tanto la cantidad de clientes como los nuevos servicios de terceros operadores. En Colombia, donde también era el mayor operador, pasó a tener de 60 a 48%[7] del mercado después de la aplicación efectiva de regulación a su filial Claro.

Pero en México, una década después de la apertura del sector, la competencia completa representa sólo 30% del mercado frente a América Móvil, hay empresas que salieron (Nextel, Iusacell), otras llegaron a invertir como AT&T que inyectó 5,600 mdd en su tercer desembarco en el país y jugadores como Movistar que solo se quedaron con una posición comercial.

[1] Ingresos anuales del sector móvil de telecomunicaciones 2021, Banco de Información de Telecomunicaciones, IFT

[2] Ingresos anuales 2021 Telcel, Banco de Información de Telecomunicaciones, IFT

[3] https://cable.com/

[4] México, Honduras, Uruguay, Chile, Brasil, Colombia, Ecuador, Perú, Nicaragua, Guatemala, El Salvador, Paraguay, Argentina, Belice, Costa Rica, Bolivia y Panamá

[5] WB 2022

[6] Carlos Urzúa & David Rivera, Empresas con poder de mercado y el bienestar social en México, 2011

[7] Participación de mercado de suscriptores móviles 2013 & 2023, GSMA Intelligence

Las opiniones expresadas son responsabilidad de sus autoras y son absolutamente independientes a la postura y línea editorial de Opinión 51.

Comments ()